A Thoughtful Start to 2026

Thank you to our clients, colleagues, and community for the continued trust in Property Cayman. We aim to do you proud.

The transition from Q4 into Q1 has been a natural one. After a strong finish to the year, momentum carried through much of Q1, and the market has now settled into a more measured pace, reflecting both seasonal patterns and a shift toward more considered decision-making. That, in many ways, is a healthy place to be.

What continues to stand out is the consistency of Cayman’s appeal. Across all segments, buyers remain focused on what we have to offer: safety, quality, stability, and long-term value.

At Property Cayman, we remain committed to providing honest advice and thoughtful guidance, no matter the stage of your property journey.

We look ahead with quiet confidence, and as always, we’re here whenever you need us.

A Market Recalibrating with Confidence

As we moved through the opening months of 2026, the Cayman Islands property market began transitioning from the conviction-driven rally into a more measured and deliberate pace. This shift was both expected and healthy.

Following a period where the new stamp duty policy brought forward a number of decisions ahead of the close of Q4, this momentum carried into much of Q1, particularly within the CI$2m–CI$3m/US$2.4m-US$4.2m range, where buyers continued to position for Permanent Residency qualification under the current framework.

With proposed changes now expected later in 2026 (potentially as early as May), this window has remained open longer than initially anticipated, sustaining activity in this segment and supporting transaction continuity beyond the typical post year-end slowdown. At the time of writing, there may be only a matter of weeks before PR thresholds begin to change.

Buyers in this segment are balancing urgency with intention, with activity shaped by alignment, timing, and longer-term planning. Importantly, this represents just one part of a broader and more balanced market.

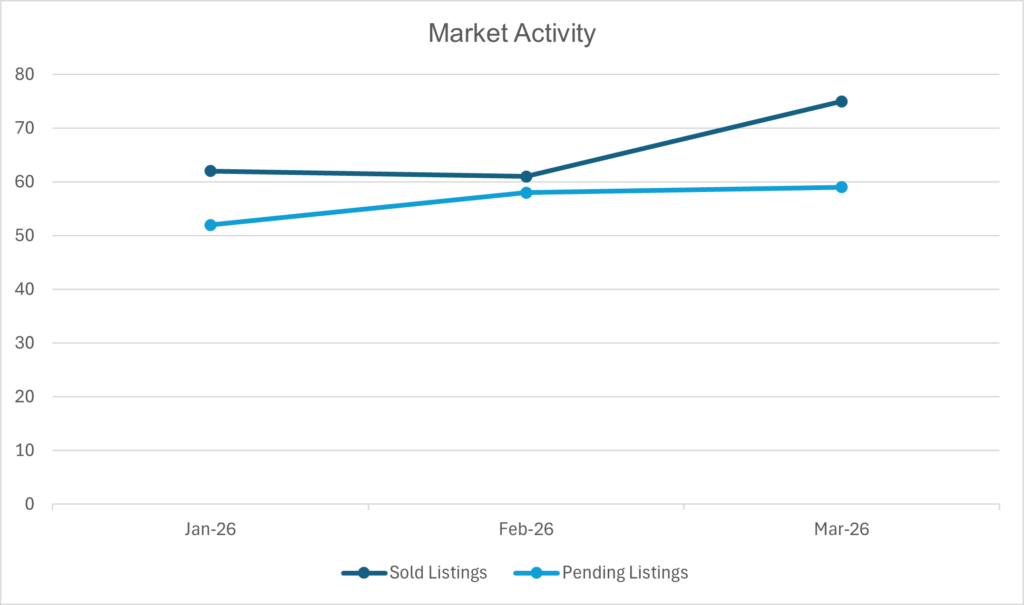

A Measured Start Following Q4 Highs

After the elevated activity seen at the end of 2025, Q1 reflected a more measured pace, particularly at the upper end of the market.

Quarter-on-quarter, transaction volumes increased slightly, rising from 195 in Q4 to 198 in Q1. Total transaction value also increased, moving from approximately US$268 million in Q4 to US$311 million in Q1.

Q1 ranked among the stronger first quarters on record, with total sales exceeding US$300 million across just under 200 transactions.

Monthly activity through the quarter followed a familiar pattern. January saw a slower start, typical for the time of year, followed by more consistent levels through February and a stronger finish in March. This points to steady buyer engagement across the quarter.

This is not a market pulling back. It is a market normalizing.

Pricing Holds, Discipline Remains

Despite several significant and record-setting transactions — including Watermark, Beachcomber, WaterColours, and Koko Kai — pricing remained resilient even as transaction volumes softened.

Average sale values increased quarter-on-quarter, rising from approximately US$1.37m in Q4 to US$1.55m in Q1. This reflects continued strength in pricing, particularly within well-located residential assets.

At the same time, market behaviour remains disciplined. Days on market held stable, moving slightly from 313 days in Q4 to 308 days in Q1. Buyers continue to prioritise due diligence and value alignment over speed.

This balance, steady pricing alongside measured absorption, remains a defining feature of the Cayman market.

From Urgency to Intent

The shift from Q4 to Q1 is best understood as a transition from urgency-driven activity to more intent-driven decision-making.

The introduction of the 10% stamp duty rate on properties above CI$2m (US$2.4m), effective 1 January 2026, has influenced transaction timing, particularly within the luxury segment.

This has been most evident in the upper-mid market, where properties aligned with the current Permanent Residency threshold continue to attract sustained interest. Rather than slowing after year-end, this segment has remained active as buyers respond to evolving timelines.

At the same time, the Permanent Residency framework remains under review, with proposed changes indicating a potential increase in both qualifying thresholds and associated fees.

In practical terms:

- At the upper end, demand remains present, though more selective

- Within the upper-mid market, a closing window of opportunity continues to support activity

- At entry and sub-threshold levels, demand remains locally driven, with limited supply supporting pricing

As with previous policy transitions, the market is responding thoughtfully. Buyers are adjusting expectations and timelines, while sellers are becoming more focused on positioning and pricing within a shifting landscape.

Collaboration Beyond Transactions

At the end of Q4, Property Cayman is proud to have played an active role in industry discussions that led to meaningful outcomes, including:

- The introduction of a CIREBA-supported grant for first-time Caymanian buyers

- The proposal that a portion of the increased stamp duty be directed toward the National Housing Development Trust (NHDT)

We remain actively engaged including through ongoing Task Force discussions, with industry stakeholders and Government, with a shared focus on supporting long-term market stability while maintaining pathways into homeownership. Significant announcements will be made within weeks.

Alongside these bigger picture efforts, Property Cayman’s community initiative, Property Cayman Cares, has now raised over CI$250,000 and has committed a portion to support ARK’s mentoring and homebuilding programmes, an initiative that remains deeply important to us and one we are committed to growing further.

In parallel, continued collaboration across industry and Government, including through Cayman Islands Real Estate Brokers Association, is helping support a more inclusive and sustainable market.

These are all important steps in strengthening the broader market ecosystem.

A Market That Continues to Attract

Against a backdrop of continued global and regional uncertainty, Cayman’s reputation as a safe, stable, and well-regulated jurisdiction continues to resonate strongly.

In periods where clarity and security matter most, Cayman continues to attract long-term capital and residents seeking certainty rather than speculation.

At the same time, market conditions are not uniform across all segments.

While the upper end continues to drive overall transaction value, the mid and entry-level segments remain defined by limited supply and sustained local demand. Well-priced properties in these segments continue to attract strong interest, often with shorter decision cycles.

The relationship between high, mid, and entry-level markets remains an important balance, one that Government continues to focus on carefully.

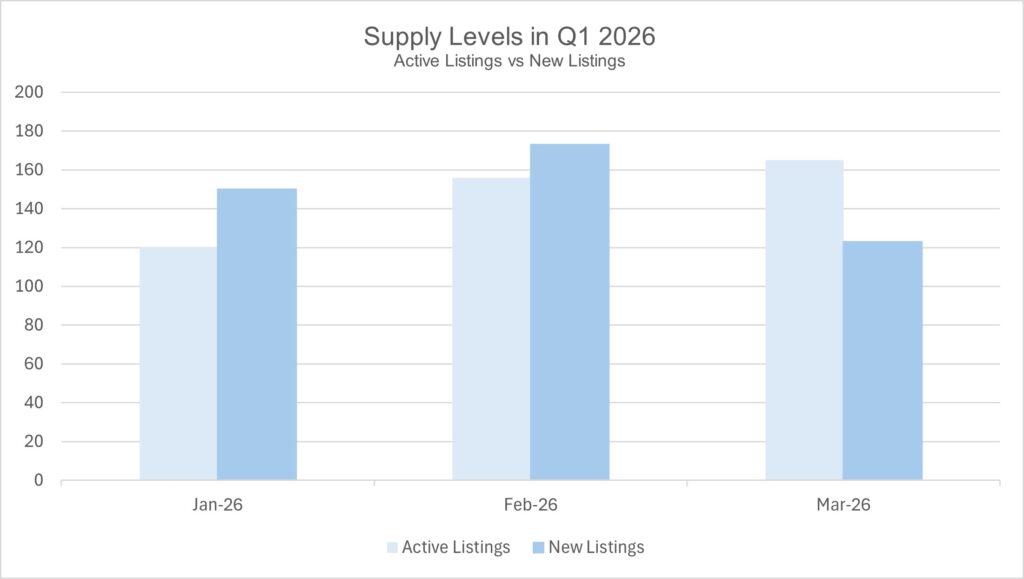

Steady Foundations, Tightening Supply

The structural foundations of the market remain strong.

Residential property continues to dominate activity, with demand focused on well-located, well-built homes offering both lifestyle and long-term value.

New listings increased notably in Q1, rising from 348 in Q4 to 446 in Q1. This reflects a clear increase in supply entering the market at the start of the year.

While this adds more choice for buyers, supply at more accessible price points remains limited, continuing to support pricing in those segments.

At the same time, nearly half a billion dollars of property entered contract during the quarter, the highest level on record, reinforcing continued forward momentum.

Looking Ahead to Q2 2026

As we look toward Q2, the expectation is for continued stability.

Before a more defined adjustment phase begins, activity within the PR threshold segment (currently in the CI$2m–CI$3m range US$2.4m-US$4.2m) is likely to see a final period of heightened activity.

The upper end is expected to remain steady, while other segments may continue at a more measured pace. Overall demand remains in place, with buyers focused on long-term positioning.

Pricing is expected to remain firm in key segments where supply remains constrained and quality remains high.

Final Thoughts

If Q4 2025 was defined by conviction, Q1 2026 has been defined by composure.

The market has not stepped back. It is adjusting. It is absorbing a period of elevated activity, responding to policy changes, and moving forward with clarity.

This is a strong place to begin the year.

This is of course a broad overview of the market. For guidance tailored to your personal circumstances, we are always happy to provide a more personalized analysis.

Recent Comments