Steady Winds, Clearer Skies

The third quarter brought subtle but significant shifts across Cayman’s property landscape, from interest rate relief to renewed buyer confidence.

Cayman’s property market has always moved at its own tempo: steady, intentional, quietly confident. As we closed Q3, that rhythm continued with just a little more lift beneath it.

After nearly two years of rising borrowing costs, the tide has finally turned. Interest rates eased through the quarter, with local banks following suit, and that small adjustment has made a meaningful difference. It hasn’t triggered a rush. Cayman doesn’t do ‘rush’. But it has nudged the market forward.

Overall, enquiries picked up, viewings stayed steady, and conversations started turning into commitments again. Buyers are re-engaging. Sellers are meeting them there. And together, the market is quietly finding its footing.

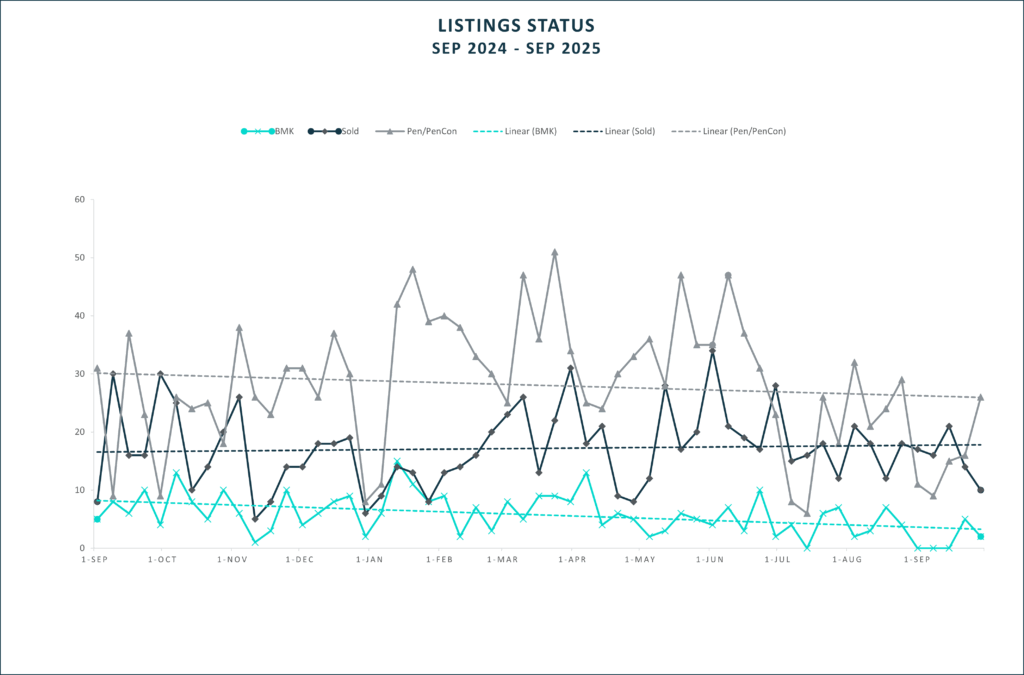

The Numbers Tell the Story

Let’s start with what we can measure.

- 302 new listings hit the market in Q3 is down slightly from 322 in Q2 but holding healthy overall.

- 185 properties sold, compared to 226 the previous quarter.

- Total sales volume reached US$193 million, about 30% lower than Q2, but largely a reflection of fewer ultra-luxury closings and the typical summer slowdown.

- Average price settled around US$1.04 million, supported by strength in the mid-market.

- Days on market fell to 313, from 416 in Q2, a clear sign that pricing and expectations are better aligned.

Inventory has remained stable at roughly 1,168 active listings, almost identical to September last year. That consistency alone speaks volumes: Cayman’s market isn’t chasing headlines; it’s setting its own.

Across all market sectors, pricing continues to move at a sustainable pace. The rate at which property pricing was increasing has slowed compared to last year. This is to say there’s still upward pressure on pricing but at a more sustainable pace. Another sign we have found a groove.

A Shift in Sentiment

The small drop in interest rates, now hovering near 7.25%, was enough to change the mood.

Financed purchases increased modestly, particularly in the sub-$2 million range, while cash buyers continued to anchor the upper end of the market.

The difference this quarter wasn’t volume, it was tone. Buyers became more decisive, sellers more grounded. Most sales closed within 15% of list price, a sign that the gap between expectation and reality is narrowing.

The mid-market carried much of the momentum. Condos and raw land between $300,000 and $800,000 remained the most active slice, as buyers based in Cayman (residents) sought attainable investments with solid long-term value.

At the higher end, activity eased, as it typically does in summer. Four luxury transactions closed this quarter, compared to five in the same period last year. But with a projected busy winter season ahead, this pause feels less like a slowdown and more like a deep breath before a new wave.

What We’re Seeing on the Ground

The market continues to favour well-presented, move-in-ready homes. Starting from scratch remains a challenge. Construction costs, bank approvals, significant planning delays, and inspection timelines are still deterrents for many would-be builders. The simple approach is to not lose faith but simply add 15% miscellaneous costs to your budget and 6 months timeline to any expectation.

This reality continues to support the value of existing homes. Buyers know what they want and act when they see it. Sellers who price for today, not yesterday’s optimism, are closing faster.

On the rental side, demand remains strong, especially for modern, well-located properties suited to professionals and short-term visitors. Tourism strength continues to ripple through investment appetite.

Highlights of the Quarter

- Condo market: Average time to sell rose to 186 days, up from 136 a year ago, though prices continued their steady climb. The top sale, a US$8.25 million Salt Creek home, showed that premium, well-positioned properties still command premium values.

- Land: Up about 1% year-to-date, with measured activity in the eastern districts and a handful of long-term investors re-entering the conversation.

- Luxury: Steady, not sleepy. Cayman’s global reputation for stability and lifestyle appeal continues to attract serious interest, even when buyers take their time.

- Mid-market: The backbone of activity. Financing confidence and improved rate sentiment made this segment the most dynamic of the quarter, yet supply is diminishing.

Calm Seas, Clear Horizons

This year’s so-called “slow season” hardly lived up to the name. Summer stayed busy, and as we move through October, storm-free so far (knock on wood, praise the Lord, and a big hallelujah), the market feels balanced, confident, and quietly optimistic.

We expect that balance to continue and momentum to build through Q4. A few high-end listings may adjust downward as the season resets, but overall supply below US$1 million will likely tighten. Rate relief should keep the mid-tier moving along, while the luxury segment readies for its usual end-of-year momentum.

Looking Ahead

Heading into the final quarter, three themes stand out:

- Renewed Confidence. Lower lending rates bring energy back into the conversation.

- Selective Strength. The luxury sector remains strong. Cayman continues to attract buyers who value lifestyle and long-term stability.

- Affordability Pressure. First-time Caymanian buyers are still navigating a tough environment. We’ll continue to champion access and opportunities for locals.

Final Thoughts

If Q2 was about holding steady, Q3 was about subtle acceleration.

Lower rates gave the market a gentle push, but Cayman’s real strength continues to be its maturity — its ability to adapt without overreacting.

We’ve made it through another quarter of calm seas, steady progress, and small, meaningful gains. And as ever, the message remains the same: in Cayman real estate, time in the market beats timing the market, every time.

Whether you’re buying, selling, investing, or simply planning your next move, our role is to help you read between the numbers and act with confidence. Let’s talk about strategy and chart what’s next.

(Please note that this is a broad analysis of the overall market. Please reach out for a bespoke detailed report tailored to your personal property journey).

Recent Comments